Debt is the lifeblood of the financial system. It turbocharges growth, as borrowing money pulls future consumption or investment into the present. At the national level, countries can take on debt to finance major government projects or to stimulate economic growth.

However, borrowed money must be repaid, which reduces consumption and investment in the future. One dollar borrowed today means one less dollar available for spending when that debt reaches maturity. Debt servicing costs – i.e. interest – also reduce cash flow available for consumption or investment.

Debt Overhang

As a country’s debt becomes larger, the government allocates more spending towards repayment. Repayment reduces the money available for government projects and social programs. The market also perceives these countries as having more credit risk, forcing creditors to demand higher interest rates as compensation.

Additionally, the pricing of sovereign debt influences the price of private-sector debt. A private borrower would pay the base government interest rate plus a risk premium based on their credit quality. So, riskier sovereign debt creates higher interest rates in the private sector. High risk premiums hinder business investment, citizens’ borrowing ability, and intensify national indebtedness.

Zombie banks, which are technically insolvent due to prior credit losses, can also restrict growth because they often require government support – pulling spending from other priorities – while their ability to lend is severely curtailed due to insolvency. Keeping a zombie bank alive costs many billions of dollars in government spending that should be better utilized elsewhere.

Zombie banks also promote the suppression of economic competition and new investment. Capital effectively frozen in loans to inefficient legacy companies is better allocated towards newer, more competitive market entrants. Japan and Europe kept insolvent banks afloat after their economic crises, which slowed down their respective recoveries. They also suffered catastrophic economic downturns and still retained the distressed loans made by banks.

At a certain level of debt, servicing existing debts becomes so costly that further borrowing becomes impossible or cost prohibitive. This distressing situation is known as “debt overhang”. Countries in an overhang are trapped in a vicious low growth cycle in which a disproportionate amount of revenue is used to repay existing debts.

Overhangs create an intense negative cycle where less funding makes it even harder to climb out of the deficit. Unfortunately, there are no easy solutions. The state can raise revenue by raising taxes or reduce spending by cutting programs, both of which are politically unpopular and harm economic growth. Another strategy is to default and try to reschedule or restructure their debts, which severely limits borrowing ability and causes borrowing costs to soar. If the debt is denominated in the state’s domestic currency, the central bank can “print” the money to pay it back, though doing so causes hyperinflation and instability.

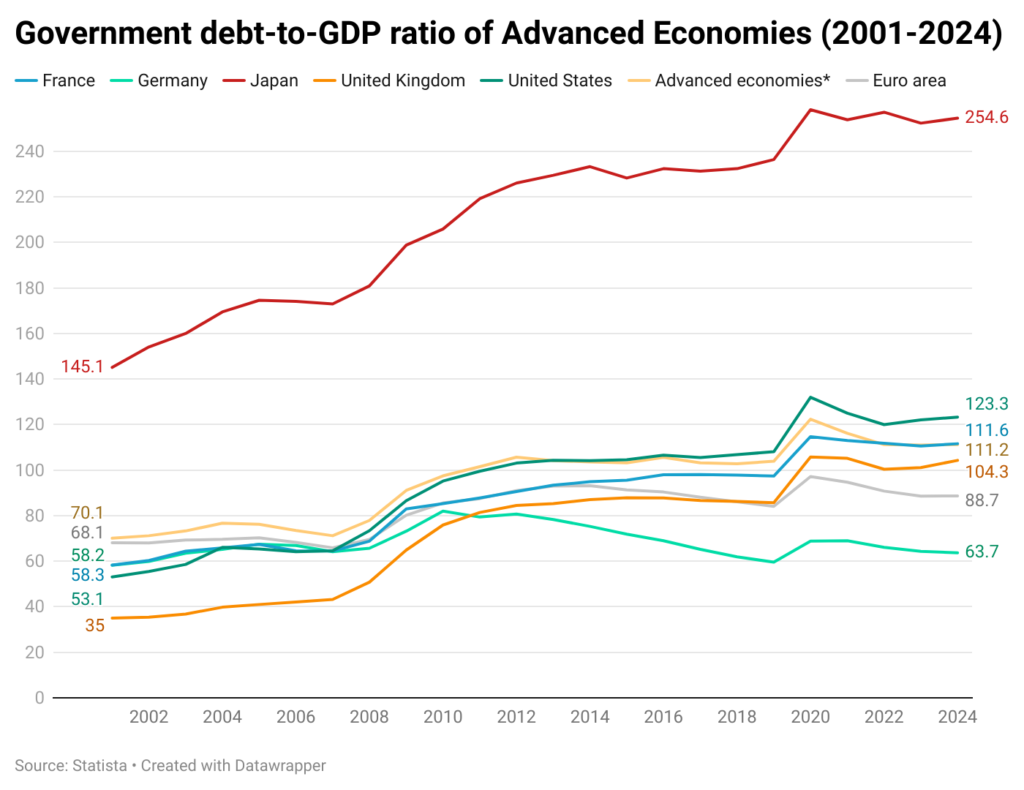

Advanced economies around the world have been facing a debt overhang in recent years.

This high debt-to-GDP ratio is incredibly dangerous for developed economies. It means that economic output grows slower than debt levels. Left unchecked, many of these first-world countries will find themselves in a brutal debt overhang.

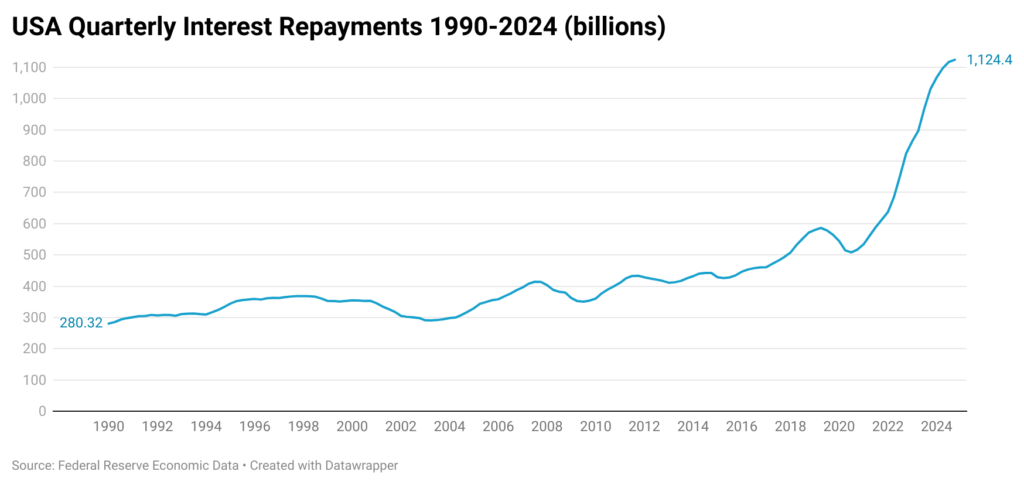

Over the last 5 years, American federal spending on interest payments has skyrocketed. The US government spent 1 trillion dollars on repayment expenditures in 2024, more than double the dollar value in 2020.

The continuation of large budget deficits has led to higher debt levels and rising interest rates, creating difficulties for America in servicing debt and causing a higher dollar value in interest repayment.

As a result, credit rating agencies have downgraded United States debt from AAA to an AA+ rating. But Treasury bonds, backed by America’s position as the undisputed global economic leader, are in high demand globally.

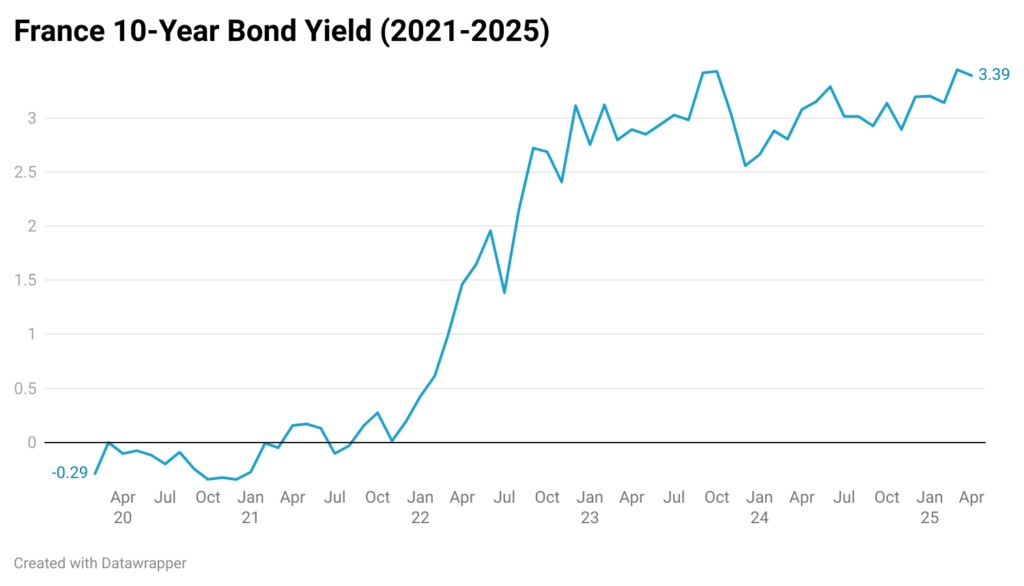

But other first-world nations are not as safe. In particular, France is experiencing one of the worst debt crises in its modern history. As they continued taking on more debt over the last couple years, bond yields skyrocketed from -0.3% in 2022 to 3.4% in 2025.

France’s political instability has exacerbated its indebtedness, which started when President Emmanuel Macron dissolved the French Parliament in June. Fears of political turmoil rose more in early December when the National Assembly ousted Prime Minister Michel Barnier’s government, halting his deficit reduction plan.

As the current coalition struggles to make progress, investor appetite for French government bonds will continue to decrease. Creditors will demand higher risk premiums as compensation for lending to an unstable government. These higher borrowing costs make it harder for the French government to reduce its deficit, starting the debt spiral.

Vietnam Sovereign Debt

Advanced economies like the United States are considered safer investments due to an established economic system and long-term productivity. Naturally, their credit is rated investment-grade (AAA-BBB), and viewed favorably by the market. However, other developing countries have the potential for more economic and sovereign debt growth.

These countries issue low-grade debt instruments (BB – D) but offer higher interest rates as compensation. As their economic situation improves, the value of the debt they issue rises. Buying debt from developing countries can be lucrative, but there are some drawbacks.

Structural issues in emerging markets block many pathways to economic growth. Many developing nations, especially in Africa and South America, become victims of government corruption, the rule of man as opposed to the rule of law, and rigid restrictions on economic and political freedom. These obstacles are usually rooted deep in the culture and take decades to overcome. They contribute to a lack of foreign direct investment and most importantly, a lack of confidence in issued debt.

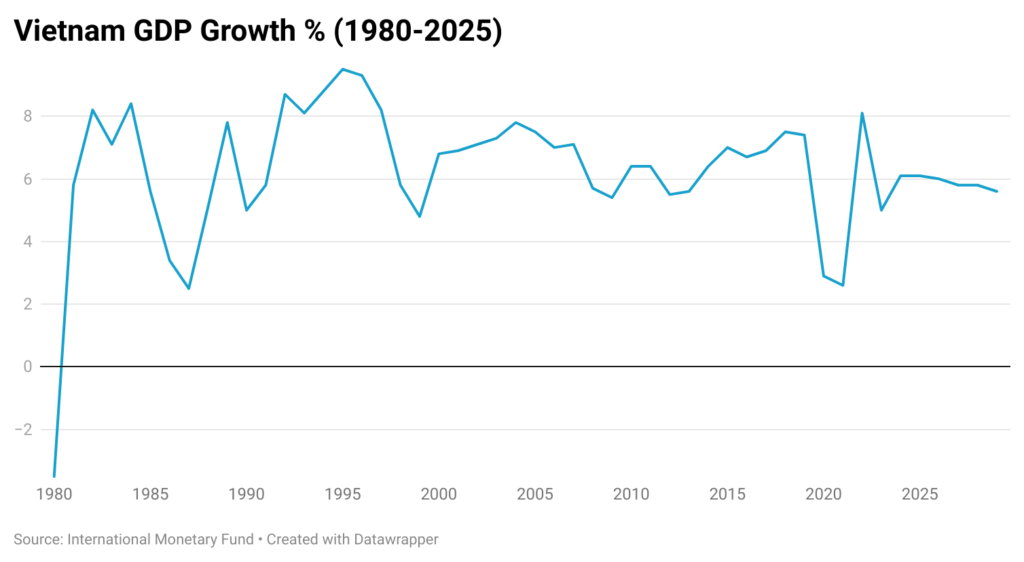

Among developing countries with a framework conducive to growth, Vietnam looks to be properly positioned for long-term growth. Its GDP rose by nearly 7% in 2023, a strong sign of continued prosperity for a country that first introduced economic reform in 1986. Vietnam’s economy was also very resilient to the coronavirus pandemic, rebounding remarkably quickly and effectively.

As a one-party country, Vietnam fell victim to poor central planning by the socialist government after the war. It led to increased economic disparity, causing political unrest. Citizens are motivated to revolt against the government as their quality of life declines, especially in authoritarian regimes. By the 1980s, it was clear that development strategies used by communist nations like the Soviet Union and Vietnam were restrictive and outdated.

To alleviate the economic hardship of its citizens, Vietnam shifted away from state-owned enterprises and introduced an open-market policy. By reducing restrictions on market participation, the government stimulated activity in the private sector, setting a foundation for future growth.

Vietnam’s government also removed restrictions on foreign trade and adopted an export-oriented strategy that persists today. Implementing free trade swayed multinational corporations to start operating in Vietnam. The private sector’s access to international markets, foreign investment, and new technology increased. By creating an efficient economic framework, liberalization turned Vietnam from a high-poverty country to a middle-income economy within one generation. Over time, the reforms introduced in 1986 have helped Vietnam’s economy prove itself as a secure source of growth.

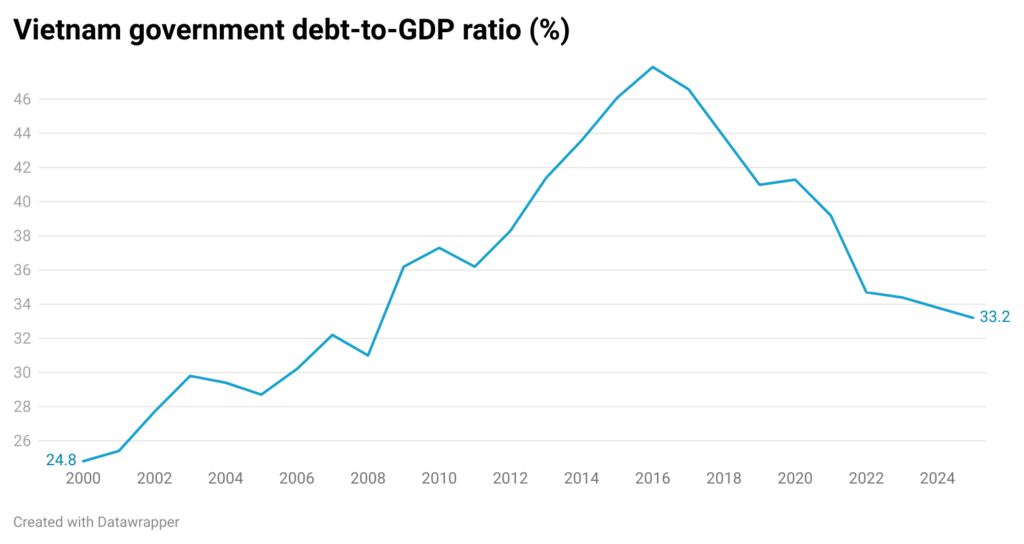

As a benefit of Vietnam’s stability, they have become one of the largest foreign direct investment collectors in South Asia. Additionally in 2022 and 2023, the main rating agencies upgraded Vietnam’s rating from BB/Ba3 to BB+/Ba2, reinforcing confidence in a positive future. Vietnam also has a low debt-to-GDP ratio of 33%, so creditors will feel secure knowing that there is low risk of default or overhang at current levels.

Despite this positive outlook, there are some obstacles to overcome before Vietnam develops into a high-income country. Mainly, their economy relies too much on trade revenue. Exports account for close to 95% of Vietnam’s economy, increasing negative exposure to shock events in global trade markets. The international implementation of protectionist policies can also hinder Vietnam’s future economic performance. Specifically, the United States has started raising tariffs on some of its largest trading partners. Considering America commands a significant share of Vietnamese exports, these tariffs will cause large fluctuations in national income. The best solution for Vietnam is to diversify global trade partnerships to become more resilient to shaky macroeconomic conditions. Additionally, industrial growth will increase citizens’ income, improving the domestic demand for Vietnamese products and decreasing reliance on foreign demand.

As Vietnam’s economy has grown, so has middle class income and quality of life. Universal health coverage has risen above the global average, and primary education rates sit above 98%. As of 2023, Vietnamese unemployment fell to under 3%. Citizens have access to electricity and cleaner water. Vietnam’s average income has risen over time, and there is also high female labor participation, which increases the workforce’s potential.

Improving quality of life and education in particular increases the skill of Vietnam’s labor base, boosting productivity and innovation. A skilled workforce has the capacity to both expand into high-value industries and invent original business ideas. It attracts domestic and foreign investment and expands private sector participation. In the future, this will amplify Vietnam’s economic growth. As technological advancements are made over time, Vietnam’s economy will integrate into global supply chains and become a promoter of new industry.

Another way Vietnam can develop its economy further is by increasing its presence in high-tech industries. The country has already been expanding into chip manufacturing as a result of American-Chinese trade wars. If divisive trade policies prevail around the globe, Vietnam can expand into high-tech and digital industries as a neutral party. This will make its economic infrastructure invaluable to the rest of the world. Shifting from low-value to high-value industries that are poised for growth creates a solid foundation for Vietnam to become an advanced economy.

Vietnam has also been making progress in renewable energy. As an attendee of COP27, it made many pledges to reduce emissions and deforestation. Over 10% of electricity comes from renewable resources. As their economy continues to grow, sustainable companies will look to Vietnam as a destination for eco-projects, furthering their green agenda. By consistently meeting long-term environmental and economic development goals, Vietnam will transition into a high-income country issuing highly-rated sovereign debt within 25-30 years.

Argentina Debt Recovery

Argentina has a checkered past as a credit risk. Chronic fiscal deficits and rapid money printing by the central bank caused a massive inflationary crisis and destroyed investor confidence in Argentina. A debt default in 2001 heightened the crisis. Even after multiple debt restructurings in the next two decades, high debt and inflation still afflicted their economy. But with President Javier Milei’s administration overseeing restrictive spending and fiscal debt repayment policies, Argentina has finally started climbing out of financial distress; even managing to run a budget surplus last year.

Additionally, Argentina has displayed signs of growth in the past and has access to many resources and industries that can increase productivity. It has a solid foundation to become a developing country and has started tracking toward economic growth, paving the way for future high-rated sovereign debt.

Hyperinflation has consistently been a main driver behind Argentina’s economic distress. It has been one of Argentina’s most persistent problems since the late 1980s. When the central bank started printing money to cover budget deficits, the value of the peso plunged, and inflation soared to over 3000%.

Hyperinflation causes the price of goods to fluctuate heavily. Besides affecting consumer spending and citizens’ quality of life, it harms business investment and government spending. Corporations, especially multinationals, have no incentive to operate in an environment where production costs swing wildly from year to year.

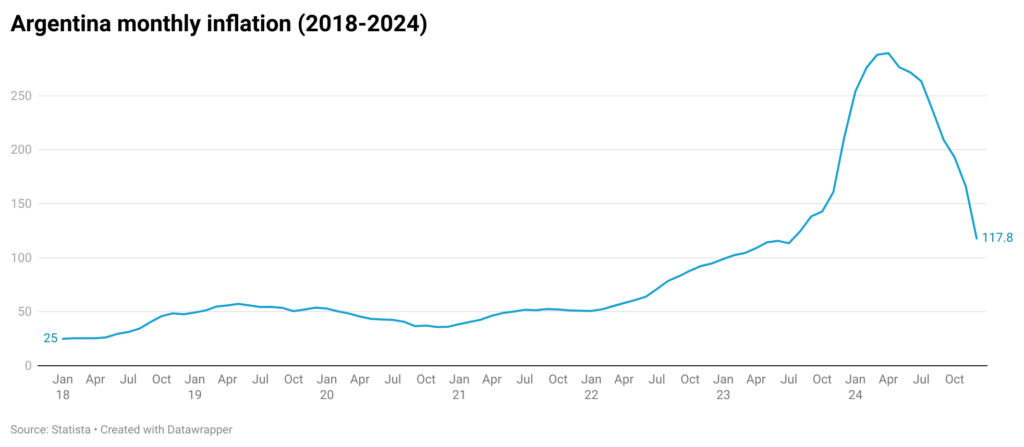

Foreign direct investment catalyzes economic growth, especially in undeveloped countries with high potential and low domestic investment. Unfortunately, hyperinflation has discouraged investors from injecting capital in Argentina’s industries for a long time. But thanks to President Milei’s policies, Argentina has started a turnaround. In January 2025, annual and monthly inflation in Argentina dropped to 84.5% and 2.2%. As government policies continue to bring it down, Argentina’s most promising sectors will start to accumulate capital from foreign contributions.

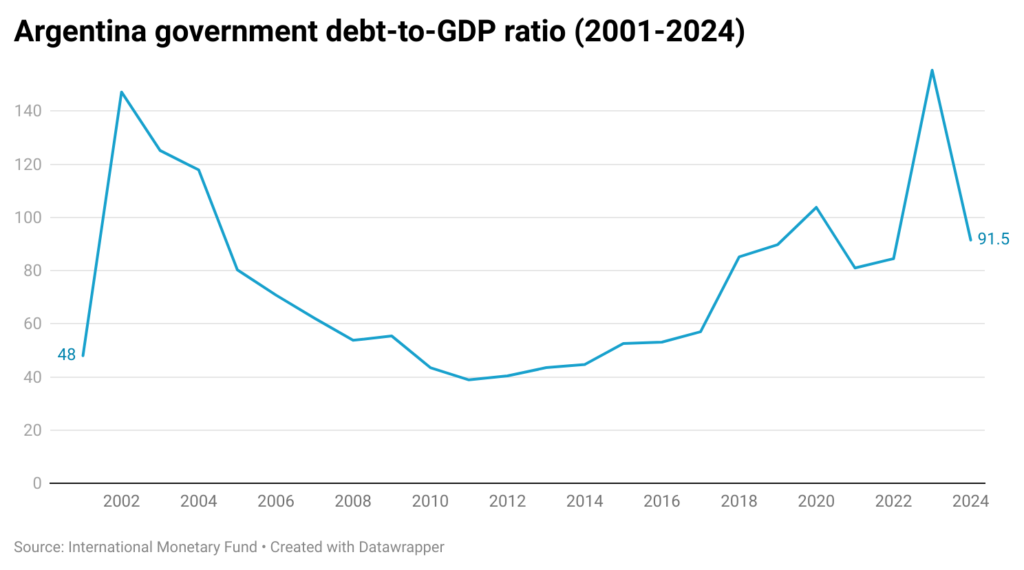

Argentina has also been steadily curbing astronomically high debt levels. Its historically large debt-to-GDP ratio has been steadily decreasing over the last year.

Much of Argentina’s economic progress has resulted from President Milei’s fiscal policies. Hard spending cuts introduced by his administration have removed the economy’s spending power but drastically improved Argentina’s indebtedness. While spending cuts will hurt corporations and citizens in the short term, it was necessitated by years of flawed fiscal strategies. Fully reversing Argentina’s deficit will bring the country more economic prosperity in the future than continuing to produce budget deficits and drowning in debt.

Since Milei took office in December 2023, Argentina had a debt-to-GDP ratio of 155%. Now, it sits at a much healthier 91.5%. These spending cuts have also had a positive effect on Argentina’s central bank policies. It allowed the central bank, BCRA, to end a long-standing practice of financing fiscal deficits, a key source of hyperinflation and currency devaluation. They also cut the benchmark interest rate from 126% down to 29%. In just 15 months, Milei has started fixing issues that have been plaguing Argentina for decades and opening channels for economic growth.

As the BCRA lowered borrowing costs by cutting interest rates, they also improved Argentina’s monetary position and liquidity. In January, five international banks conducted a $1 billion repurchase agreement with the BCRA. The interest shown by foreign lenders is a precursor to the stabilization of Argentina’s international liquidity and the removal of capital restrictions, paving the way for economic growth.

Additionally, monetary aggregate M2 grew by 3.4% last year, indicating a rise in Argentina’s money supply. Much of this growth came from private investment, where private sector loans rose by 6.5%. Currency circulation also increased by 4.2%, reflecting a sentiment of inflation decline and trust in liquid assets among Argentinian individuals and corporations. They can use this money to invest in themselves and the economy rather than keep it locked up in rigid assets.

President Milei’s next step needs to be boosting business investment and tapping into Argentina’s natural resources and skilled labor force to improve the real economy. Incentivizing investment in Argentina’s industries will show creditors that in the long-term, they will be a stable outlet for foreign contributions.

Geographically, Argentina has vast amounts of land containing gas and lithium deposits. This creates high economic potential in food production, resource mining, renewable resources, and oil & gas exploration. While Milei has started offering tax breaks for investments larger than $200 million, more strategies need to be implemented to reap the benefits of growing economic institutions.

Pushing for more domestic labor in high-growth industries can boost investment in Argentina while improving citizens’ living conditions. Offering economic incentives for hiring Argentine workers will help reduce unemployment and poverty rates. It also brings foreign cash into Argentina’s economy by increasing individuals’ income. Implementing these strategies and maintaining sound fiscal and monetary policies will help take Argentina from a financially distressed country to an economic leader in South America.