Growth stocks — and specifically large-cap tech stocks led by the FAANGs — have utterly crushed value stocks of late. It’s been the dominant theme of the past five years. Even the first quarter of 2018, which saw Facebook engulfed in a privacy scandal, saw growth outperform value.

| Sector | Benchmark | Qtr. Return |

|---|---|---|

| Large-Cap Growth | S&P 500 Growth | 1.58% |

| Large-Cap Stocks | S&P 500 | -1.22% |

| International | MSCI EAFE Index | -2.19% |

| Utilities | S&P 500 Utilities | -3.30% |

| Large-Cap Value | S&P 500 Value | -4.16% |

| Real Estate Investment Trusts | S&P U.S. REIT Index | -9.16% |

| Master Limited Partnerships | Alerian MLP Index | -11.22 |

Value stocks in general underperformed, and the cheapest of the cheap — master limited partnerships — got utterly obliterated.

So, is value investing dead?

Before you start digging its grave, consider the experience of Julian Robertson, one of the greatest money managers in history and the godfather of the modern hedge fund industry. Robertson produced an amazing track record of 32% compounded annual returns for nearly two decades in the 1980s and 1990s, crushing the S&P 500 and virtually all of his competitors. But the late 1990s tech bubble tripped him up, and he had two disappointing years in 1998 and 1999.

Facing client redemptions, Robertson opted to shut down his fund altogether. His parting words to investors are telling.

The following is the Julian Robertson’s final letter to his investors, dated March 30, 2000, written as he was in the process of shutting down Tiger Management:

In May of 1980, Thorpe McKenzie and I started the Tiger funds with total capital of $8.8 million. Eighteen years later, the $8.8 million had grown to $21 billion, an increase of over 259,000 percent. Our compound rate of return to partners during this period after all fees was 31.7 percent. No one had a better record.

Since August of 1998, the Tiger funds have stumbled badly and Tiger investors have voted strongly with their pocketbooks, understandably so. During that period, Tiger investors withdrew some $7.7 billion of funds. The result of the demise of value investing and investor withdrawals has been financial erosion, stressful to us all. And there is no real indication that a quick end is in sight.

And what do I mean by, “there is no quick end in sight?” What is “end” the end of? “End” is the end of the bear market in value stocks. It is the recognition that equities with cash-on-cash returns of 15 to 25 percent, regardless of their short-term market performance, are great investments. “End” in this case means a beginning by investors overall to put aside momentum and potential short-term gain in highly speculative stocks to take the more assured, yet still historically high returns available in out-of-favor equities.

There is a lot of talk now about the New Economy (meaning Internet, technology and telecom). Certainly, the Internet is changing the world and the advances from biotechnology will be equally amazing. Technology and telecommunications bring us opportunities none of us have dreamed of.

“Avoid the Old Economy and invest in the New and forget about price,” proclaim the pundits. And in truth, that has been the way to invest over the last eighteen months.

As you have heard me say on many occasions, the key to Tiger’s success over the years has been a steady commitment to buying the best stocks and shorting the worst. In a rational environment, this strategy functions well. But in an irrational market, where earnings and price considerations take a back seat to mouse clicks and momentum, such logic, as we have learned, does not count for much.

The current technology, Internet and telecom craze, fueled by the performance desires of investors, money managers and even financial buyers, is unwittingly creating a Ponzi pyramid destined for collapse. The tragedy is, however, that the only way to generate short-term performance in the current environment is to buy these stocks. That makes the process self-perpetuating until the pyramid eventually collapses under its own excess. [Charles here. Sound familiar? Fear of trailing the benchmark has led managers to pile into the FAANGs.]

I have great faith though that, “this, too, will pass.” We have seen manic periods like this before and I remain confident that despite the current disfavor in which it is held, value investing remains the best course. There is just too much reward in certain mundane, Old Economy stocks to ignore. This is not the first time that value stocks have taken a licking. Many of the great value investors produced terrible returns from 1970 to 1975 and from 1980 to 1981 but then they came back in spades.

The difficulty is predicting when this change will occur and in this regard, I have no advantage. What I do know is that there is no point in subjecting our investors to risk in a market which I frankly do not understand. Consequently, after thorough consideration, I have decided to return all capital to our investors, effectively bringing down the curtain on the Tiger funds. We have already largely liquefied the portfolio and plan to return assets as outlined in the attached plan.

No one wishes more than I that I had taken this course earlier. Regardless, it has been an enjoyable and rewarding 20 years. The triumphs have by no means been totally diminished by the recent setbacks. Since inception, an investment in Tiger has grown 85-fold net of fees; more than three time the average of the S&P 500 and five-and-a-half times that of the Morgan Stanley Capital International World Index. The best part by far has been the opportunity to work closely with a unique cadre of co-workers and investors.

For every minute of it, the good times and the bad, the victories and the defeats, I speak for myself and a multitude of Tiger’s past and present who thank you from the bottom of our hearts.

Charles here. The more things change, the more they stay the same. Value will have its day in the sun again, and that day is likely here with the FAANGs finally starting to break down.

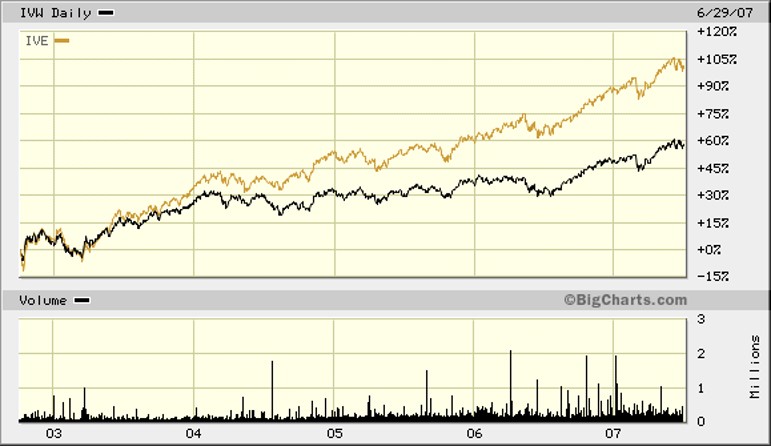

Had Robertson held on a little longer, he would have been vindicated and likely would have made a killing. Consider the outperformance of value over growth in the years between the tech bust and the Great Recession:

So, don’t abandon value investing just yet. If history is any guide, it’s set to leave growth in the dust.

This article first appeared on Sizemore Insights as Keeping Perspective: Julian Robertson’s Last Letter to Investors